Feeling uncertain about where to start with property investment is common for many new American real estate investors. The maze of loan types, credit requirements, and complex terms can make the goal of property ownership seem out of reach. By breaking down the core concepts of real estate financing, this guide offers approachable strategies and resources to help simplify your decision-making so you can move forward with clarity and confidence.

Table of Contents

- What Is Real Estate Financing? Core Concepts

- Traditional and Alternative Loan Types Compared

- How Financing Works for Investment Properties

- Requirements and Qualifications for Beginners

- Potential Risks and Financial Implications

- Common Mistakes and Choosing the Best Option

Key Takeaways

| Point | Details |

|---|---|

| Understanding Mortgage Types is Crucial | Familiarize yourself with different mortgages like Conventional, FHA, VA, and USDA loans to find options that best fit your financial situation. |

| Evaluate Risks Before Investing | Be aware of potential financial risks such as market volatility and unexpected costs to safeguard your investment strategy. |

| Conduct Thorough Comparisons | Always compare multiple financing options and loan products to ensure the best fit for your financial goals and avoid common pitfalls. |

| Prepare Financially Before Applying | Strengthen your credit and gather necessary documentation to enhance your chances of mortgage approval and better loan terms. |

What Is Real Estate Financing? Core Concepts

Real estate financing represents the strategic process that enables individuals and businesses to acquire property through structured financial mechanisms. At its core, this approach transforms complex property purchases into achievable goals by providing specialized funding mechanisms that bridge individual resources with property ownership.

The financing landscape involves multiple critical components that potential investors and homebuyers must understand:

- Mortgage Types: Traditional bank loans, government-backed programs, and specialized lending products

- Funding Sources: Banks, credit unions, private lenders, and alternative investment platforms

- Risk Assessment: Comprehensive evaluation of borrower creditworthiness and property valuation

- Loan Parameters: Interest rates, repayment terms, down payment requirements

Government programs play a significant role in expanding real estate financing accessibility. FHA loans, for instance, provide unique opportunities for first-time buyers by offering more flexible qualification standards, including lower down payment requirements and more lenient credit score considerations.

Financial institutions evaluate multiple factors when determining real estate financing eligibility, including:

- Personal credit history

- Current income and employment stability

- Debt-to-income ratio

- Property appraisal value

- Potential future investment returns

Real estate financing transforms property acquisition from an intimidating challenge into a structured, achievable financial strategy.

Pro tip: Always compare multiple financing options and get pre-approved before seriously searching for properties to understand your exact purchasing power and strengthen your negotiating position.

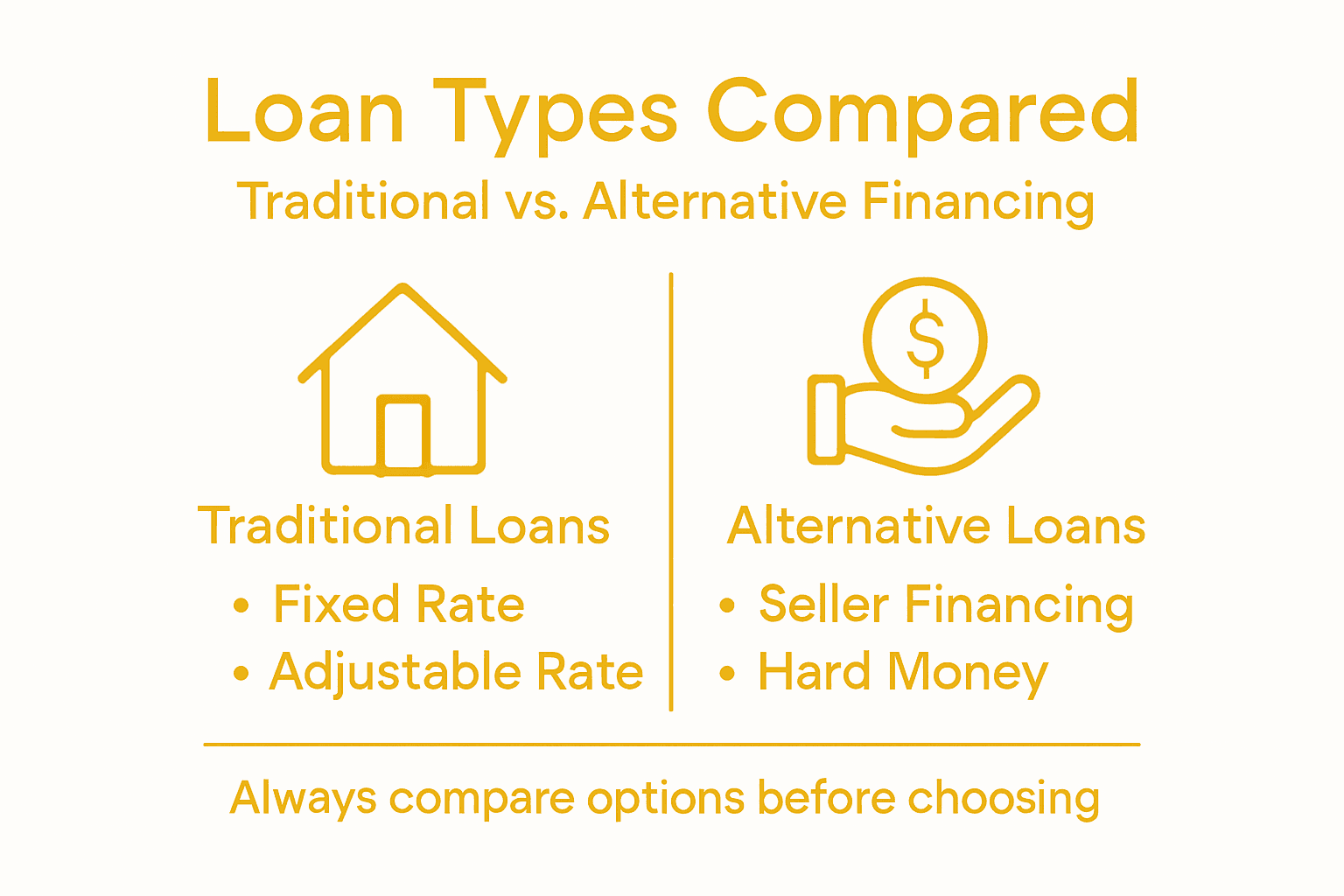

Traditional and Alternative Loan Types Compared

Real estate financing encompasses a diverse range of lending approaches, with traditional and alternative financing options presenting unique advantages and challenges for potential property investors. Traditional mortgages represent the most common pathway, involving standardized bank loans with well-established regulatory frameworks and predictable terms.

Traditional loan types typically include:

- Conventional Mortgages: Standard bank loans with fixed or adjustable interest rates

- FHA Loans: Government-backed mortgages with more flexible qualification standards

- VA Loans: Specialized financing for military veterans and service members

- USDA Rural Development Loans: Targeted financing for rural property purchases

Alternative financing arrangements offer more flexible approaches for borrowers who might not qualify for conventional lending. These options include:

- Seller Financing: Direct loan agreements between buyer and property seller

- Hard Money Loans: Short-term, asset-based financing from private investors

- Peer-to-Peer Lending: Online platforms connecting borrowers with individual investors

- Private Money Loans: Customized financing from individual or business lenders

Ownership structures differ significantly between traditional and alternative financing methods. In conventional mortgages, legal title transfers immediately, while alternative arrangements like land contracts may retain seller ownership during the loan term.

Here’s a concise comparison of traditional and alternative real estate loan types to help guide financing decisions:

| Aspect | Traditional Loans | Alternative Financing |

|---|---|---|

| Approval Process | Stringent, credit-focused | Flexible, less strict |

| Loan Structure | Standardized terms | Customized or case-specific |

| Regulatory Oversight | High, federally regulated | Limited, varies widely |

| Typical Borrowers | Prime credit, stable income | Entrepreneurs, non-traditional profiles |

| Ownership Transfer | Immediate to buyer | May remain with seller temporarily |

| Use Case | Primary residences, low-risk | Investments, unique situations |

Alternative financing can provide opportunities, but investors must carefully evaluate potential risks and legal complexities.

Pro tip: Always conduct comprehensive due diligence and consult with a real estate attorney before pursuing alternative financing arrangements to understand potential legal and financial implications.

How Financing Works for Investment Properties

Investment property financing represents a unique financial landscape that differs significantly from traditional residential mortgages. Lenders evaluate investment properties through a more complex lens, focusing on potential income generation and overall financial performance rather than just borrower creditworthiness.

Key factors lenders consider for investment property financing include:

- Rental Income Potential: Projected monthly rental revenues

- Debt Service Coverage Ratio: Ability to cover loan payments through property income

- Credit Score: Typically requiring higher scores than primary residence loans

- Down Payment: Often 20-30% compared to 3-5% for owner-occupied properties

- Cash Reserves: Demonstrating financial stability beyond the property purchase

The financing process for investment properties involves several critical evaluation stages:

- Property Income Assessment

- Comprehensive Financial Documentation

- Detailed Market Research

- Risk Profile Determination

- Loan Structure Recommendation

Unlike residential mortgages, investment property lending involves stricter regulatory standards that protect both lenders and investors. Financial institutions develop comprehensive written policies to minimize potential losses and ensure sound credit administration.

Use this summary to quickly understand key investment property financing metrics:

| Metric | Investment Properties | Owner-Occupied Homes |

|---|---|---|

| Minimum Down Payment | 20-30% of price | As low as 3-5% |

| Credit Score Needed | 700+ often required | 580-620 depending on program |

| Required Cash Reserves | Several months’ payments | Less stringent for most loans |

| Focus of Lender | Income from property | Personal borrower profile |

| Typical Loan Terms | Stricter, higher rates | Favorable, lower rates |

Investment property financing is not just about borrowing money, but strategically positioning your real estate asset for long-term financial success.

Pro tip: Always maintain detailed financial records and prepare a comprehensive business plan demonstrating the investment property’s potential profitability before approaching lenders.

Requirements and Qualifications for Beginners

Navigating real estate financing as a beginner requires understanding the key financial requirements for mortgage approval. Lenders evaluate potential borrowers through a comprehensive lens that goes beyond simple credit scores, examining multiple aspects of financial health and stability.

Critical qualification criteria for beginners include:

- Credit Score: Minimum 620 for conventional loans, 580 for FHA loans

- Debt-to-Income Ratio: Typically must be under 43%

- Employment History: Stable income for at least two consecutive years

- Down Payment: Ranging from 3.5% to 20% depending on loan type

- Cash Reserves: Ability to cover several months of mortgage payments

First-time investors and homebuyers should focus on preparing their financial profile by:

- Checking and improving credit reports

- Reducing existing debt

- Saving for down payment and emergency funds

- Gathering comprehensive financial documentation

- Getting pre-approved for mortgage financing

Mortgage application tools help navigate complex qualification processes by providing clear guidance on documentation and lending standards. Government-backed programs like FHA loans offer more accessible pathways for those with limited financial resources.

Successful financing starts with understanding your financial strengths and addressing potential weaknesses before approaching lenders.

Pro tip: Obtain a comprehensive credit report at least six months before applying for a mortgage, allowing time to address any potential issues and improve your financial standing.

Potential Risks and Financial Implications

Real estate financing involves complex financial risks that require careful understanding, extending far beyond simple loan approval. Investors and homebuyers must navigate potential challenges that could significantly impact their long-term financial health and property investment strategy.

Primary financial risks in real estate financing include:

- Market Volatility: Potential property value fluctuations

- Interest Rate Changes: Unexpected increases in borrowing costs

- Income Disruption: Challenges meeting mortgage payments

- Unexpected Maintenance Expenses: Potential financial strain

- Foreclosure Risk: Potential loss of property investment

Specific implications for borrowers involve multiple potential scenarios:

- Negative equity if property values decline

- Credit score damage from missed payments

- Potential legal complications during default

- Long-term financial recovery challenges

- Reduced future borrowing capabilities

Alternative financing arrangements carry additional unique ownership and financial risks, including unclear property titles and limited legal protections. These arrangements can expose investors to significant financial uncertainties not present in traditional mortgage structures.

Financial preparedness and thorough risk assessment are crucial to successful real estate investment.

Pro tip: Create a comprehensive financial buffer of 6-12 months of mortgage payments to protect against unexpected income disruptions or market challenges.

Common Mistakes and Choosing the Best Option

Selecting the right real estate financing requires strategic decision-making and awareness of potential pitfalls. Common mistakes can significantly derail investment plans, making thorough research and careful evaluation crucial for success.

Frequent mistakes beginners make include:

- Overlooking Total Costs: Focusing solely on monthly payments

- Ignoring Credit Requirements: Failing to prepare credit profile

- Skipping Loan Comparisons: Not exploring multiple lending options

- Underestimating Additional Expenses: Neglecting closing costs and fees

- Rushing Decision-Making: Choosing without comprehensive evaluation

Strategies for selecting the best financing option involve:

- Analyzing personal financial health

- Understanding long-term investment goals

- Comparing multiple loan products

- Evaluating total loan costs

- Considering future financial flexibility

Comprehensive loan option evaluation requires examining multiple factors beyond simple interest rates. Investors must consider loan terms, repayment flexibility, potential penalties, and alignment with personal financial objectives.

Successful real estate financing is less about finding the cheapest option and more about finding the most strategic fit for your financial journey.

Pro tip: Create a detailed spreadsheet comparing loan options, including interest rates, total costs, and potential long-term implications before making a final decision.

Unlock Your Path to Confident Real Estate Financing

Understanding the complexities of real estate financing is crucial for any beginner looking to make smart property investments. This article breaks down essential concepts such as mortgage types, financing options, qualification requirements, and potential risks. If you feel overwhelmed navigating terms like debt-to-income ratio, FHA loans, or investment property financing details you are not alone. The key challenge is turning this knowledge into actionable steps while avoiding common pitfalls.

At Bold Street AI we specialize in simplifying these challenges by connecting you with trusted, investor-friendly lenders and expert agents who can guide you through financing strategies tailored to your unique situation. Our platform offers educational resources including the Bold Academy that empower beginners to understand financing requirements and explore the best loan options. With access to curated investment opportunities and a supportive community, you will build the confidence and clarity needed to make sound financing decisions.

Explore Financing Options and take advantage of expert guidance that aligns with your goals.

Start your journey today at Bold Street AI and equip yourself with the tools, mentorship, and connections necessary to secure financing with confidence. Don’t let uncertainty hold you back when the right support is just a click away.

Frequently Asked Questions

What is real estate financing?

Real estate financing is the process that allows individuals and businesses to acquire property through structured financial mechanisms, transforming property purchases into achievable goals by providing specialized funding options.

What are the different types of mortgages available?

Common mortgage types include conventional mortgages, FHA loans, VA loans, and USDA Rural Development loans, each offering different terms and qualification criteria suited to various borrower needs.

How do lenders assess eligibility for real estate financing?

Lenders evaluate eligibility based on factors like credit history, income stability, debt-to-income ratio, property appraisal value, and potential future income from the property.

What are the risks associated with real estate financing?

Key risks include market volatility, interest rate changes, income disruptions, unexpected maintenance costs, and the potential for foreclosure if obligations are not met.

Recommended

- Financing Options for Investors: Building Wealth in Real Estate | Bold Street AI

- Role of Financing in Residential Investing Success | Bold Street AI

- Real Estate Investment Terms Explained: What Beginners Need | Bold Street AI

- Step by Step Real Estate Investing for Beginners | Bold Street AI

- real estate development software | 3D Cityplanner