Most American real estate investors quickly discover that financing is the cornerstone of building wealth through property. With over 80% of American residential investments relying on borrowed funds, understanding the choices available can make or break a new investor’s portfolio. Unpacking the real differences between conventional, private, and creative loans gives you the power to build a smarter investment strategy while avoiding costly missteps.

Table of Contents

- Defining Investor Financing In Real Estate

- Comparing Conventional, Private, And Creative Loans

- Key Loan Features And How They Work

- Lender Qualifications And Investor Eligibility

- Risks, Costs, And Tax Implications

- Mistakes To Avoid When Choosing Financing

Key Takeaways

| Point | Details |

|---|---|

| Understanding Investor Financing | Investor financing involves leveraging various capital sources to optimize property investments and generate returns. |

| Loan Comparison | Compare conventional, private, and creative financing options to find the best fit for your investment goals and risk tolerance. |

| Key Loan Features | Familiarize yourself with important loan characteristics such as loan-to-value ratios and amortization schedules to enhance investment decisions. |

| Avoid Financing Mistakes | Thoroughly understand loan terms and evaluate all costs to prevent missteps that could jeopardize financial sustainability. |

Defining Investor Financing in Real Estate

Investor financing represents the strategic capital deployment that enables real estate investors to acquire, develop, and generate returns from property investments. Real estate finance encompasses a complex ecosystem of funding mechanisms designed to help investors transform property opportunities into profitable ventures.

At its core, investor financing involves multiple capital sources including traditional bank loans, private money lending, hard money loans, and creative financing strategies. These financial tools allow investors to leverage borrowed funds to purchase properties without requiring full upfront capital. The fundamental principle underlying investor financing is using other people’s money to generate personal wealth through real estate appreciation, rental income, or property improvements.

The capital structure in real estate investing typically involves a strategic hierarchy of financial resources. Debt financing, such as mortgages and loans, provides the initial purchasing power, while equity investments represent the investor’s personal stake and potential profit margins. Sophisticated investors often blend multiple financing approaches to optimize risk management and maximize potential returns. Understanding these intricate financing mechanisms requires deep knowledge of lending requirements, interest rates, and investment property evaluation.

Pro tip: Always calculate your potential return on investment and debt service coverage ratio before committing to any real estate financing strategy to ensure financial sustainability.

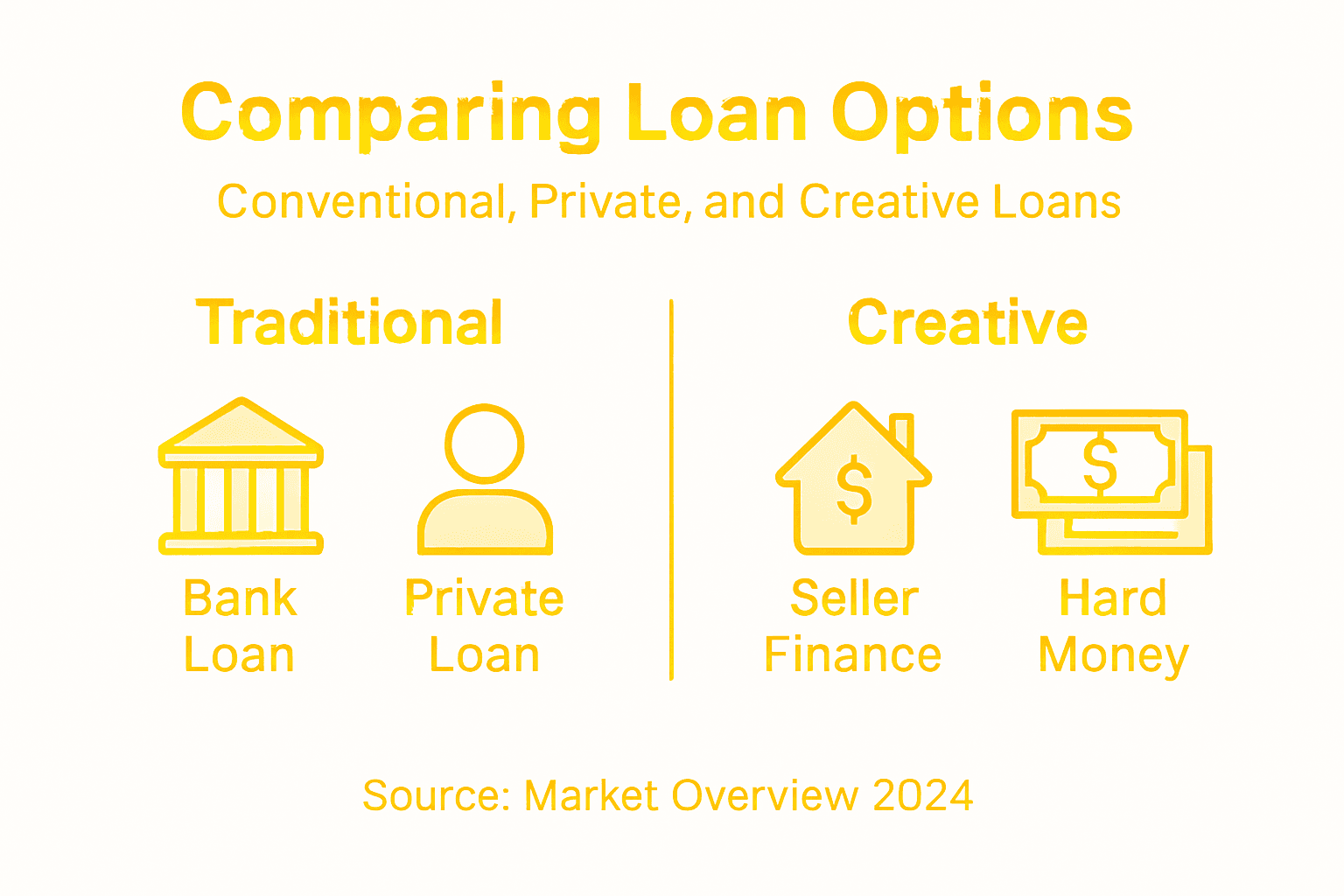

Comparing Conventional, Private, and Creative Loans

Real estate investors have multiple financing pathways, each with unique advantages and strategic implications. Commercial real estate loans represent a diverse landscape of funding options designed to match different investment scenarios and investor risk profiles.

Conventional loans remain the most traditional financing method, typically offered by banks and requiring strong credit histories and documented income. These loans feature lower interest rates and longer repayment terms, making them attractive for investors with stable financial backgrounds. In contrast, private loans emerge as a more flexible alternative, often provided by nonbank lenders who can accommodate investors with less conventional financial profiles. Private lending frequently involves higher interest rates but offers faster approval processes and more lenient qualification requirements.

Creative financing introduces innovative strategies for property acquisition. Alternative financing methods like seller financing, lease options, and hard money loans enable investors to purchase properties with minimal personal capital. These approaches often involve unique structures such as simultaneous closings or subject-to transactions, where investors acquire property titles through non-traditional mechanisms. Creative loans can be particularly powerful for fix-and-flip projects, real estate development, or situations where conventional lending proves challenging.

A comprehensive understanding of these loan types empowers investors to select the most appropriate financing strategy based on their specific investment goals, risk tolerance, and financial capacity. By strategically combining different loan structures, savvy investors can optimize their real estate investment portfolios.

Pro tip: Always conduct thorough due diligence and compare multiple loan options, analyzing not just interest rates but total borrowing costs and potential investment returns.

Here’s a side-by-side comparison summarizing the main differences between conventional, private, and creative real estate loans:

| Loan Type | Approval Speed | Typical Interest Rates | Flexibility of Terms |

|---|---|---|---|

| Conventional | Slow (2-6 weeks) | Low (3-6%) | Strict, little negotiation |

| Private | Fast (3-10 days) | High (7-15%) | Highly flexible terms |

| Creative | Varies widely | Moderate to high | Extremely creative structures |

Key Loan Features and How They Work

Real estate financing involves a complex array of strategic considerations that go far beyond simple borrowing. Real estate loan structures encompass multiple sophisticated elements designed to match investor goals with appropriate financial mechanisms.

Investors must understand key loan features that directly impact investment performance. Loan-to-value ratios represent a critical metric, determining how much capital an investor can borrow relative to the property’s appraised value. Typical commercial real estate loans offer leverage ratios ranging from 3:1 to 4:1, allowing investors to maximize potential returns while managing risk. Interest rates, loan terms, and repayment structures vary significantly across different financing products. Some loans feature traditional amortizing payments, while others offer interest-only periods or flexible balloon payment arrangements that can align with specific investment strategies.

Underwriting processes play a crucial role in loan approval, with lenders carefully analyzing project risks before committing funds. Key evaluation criteria include the development team’s capacity, projected cash flow, potential tenant creditworthiness, and broader market dynamics. Investors must prepare comprehensive documentation demonstrating their financial stability, project feasibility, and potential for generating sustainable returns. Different loan types serve specific investment stages – acquisition loans, construction loans, bridge loans, and permanent financing each address unique real estate investment requirements.

Successful real estate investors develop a nuanced understanding of these loan features, strategically selecting financing that optimally supports their investment objectives and risk tolerance.

Pro tip: Always calculate your debt service coverage ratio and compare multiple loan options to ensure the financing aligns perfectly with your specific investment strategy.

The following table provides a quick reference for key loan features and their impact on real estate investment outcomes:

| Loan Feature | Description | Impact on Investment |

|---|---|---|

| Loan-to-Value Ratio | Percent financed vs. property value | Higher ratio increases leverage |

| Amortization Schedule | Timeframe for repaying principal | Shorter term, higher payment |

| Balloon Payment | Large payment at end of term | May require refinancing |

| Interest-Only Period | Pay interest, defer principal | Lower payments, cash flow boost |

Lender Qualifications and Investor Eligibility

Navigating the landscape of real estate investment requires a deep understanding of lender qualification standards that govern financial transactions. Investors must recognize the complex framework of requirements designed to protect both lenders and borrowers in real estate investments.

Creditworthiness stands as the primary threshold for investor eligibility. Lenders meticulously evaluate an investor’s financial profile through multiple dimensions, including credit score, income stability, debt-to-income ratio, and previous investment performance. Typically, investors need a credit score of 680 or higher, consistent income documentation for the past two years, and a debt-to-income ratio below 43% to qualify for most real estate investment loans. Accredited investor status represents an additional tier of eligibility, particularly for private real estate deals, which requires a net worth exceeding $1 million or annual income above $200,000 for the past two consecutive years.

Beyond individual financial metrics, lenders assess the specific investment property’s potential. This comprehensive evaluation includes property appraisal, market comparables, potential rental income, and the investor’s proposed business strategy. Different loan types demand varying levels of documentation and financial strength. Conventional investment property loans often require larger down payments (typically 25-30%) compared to owner-occupied mortgages, reflecting the higher perceived risk associated with investment properties.

Successful real estate investors develop a strategic approach to meeting lender qualifications, understanding that financial preparation is as crucial as identifying promising investment opportunities.

Pro tip: Maintain meticulous financial records and work on improving your credit score at least 12 months before applying for an investment property loan.

Risks, Costs, and Tax Implications

Real estate investment demands a sophisticated understanding of financial risk management that extends far beyond simple property acquisition. Investors must develop a comprehensive framework for evaluating potential challenges and financial implications.

Market volatility represents a significant risk factor in real estate investments. Economic downturns, local market shifts, and unexpected property value fluctuations can dramatically impact investment returns. Investors should anticipate potential costs beyond the initial purchase price, including maintenance expenses, property management fees, insurance premiums, and potential vacancy periods. Typical additional costs range from 2% to 5% of the property’s value annually, which can significantly erode potential profits if not carefully managed.

Tax implications introduce another layer of complexity for real estate investors. Strategies such as depreciation deductions can offset income, while capital gains taxes require careful planning upon property sale. Investors must navigate intricate tax regulations, potentially leveraging strategies like 1031 exchanges to defer tax liabilities. Financial compliance risks also demand meticulous attention, with potential legal and financial consequences for improper reporting or unintentional regulatory violations.

Successful real estate investors approach risks, costs, and tax implications with a proactive, strategic mindset, treating financial management as a critical component of their investment approach.

Pro tip: Consult with a certified tax professional and create a comprehensive financial contingency plan that includes a minimum 6-month emergency fund for unexpected property expenses.

Mistakes to Avoid When Choosing Financing

Navigating real estate financing requires strategic awareness and comprehensive understanding of potential financing pitfalls. Investors must approach loan selection with meticulous attention to detail and a comprehensive risk management perspective.

Misunderstanding loan terms represents a critical error that can devastate investment strategies. Many investors overlook crucial details such as prepayment penalties, adjustable interest rate mechanisms, and hidden closing costs. Failing to comprehend the full financial implications of loan structures can lead to unexpected expenses that dramatically reduce investment profitability. Typical mistakes include selecting loans with teaser rates that spike dramatically after initial periods, or choosing financing without considering long-term cash flow implications.

Investors frequently miscalculate investment risk assessment by focusing solely on potential returns without understanding comprehensive financial exposure. Common missteps include neglecting to establish robust emergency reserves, underestimating maintenance and vacancy costs, and failing to align loan terms with specific investment strategies. Some investors choose financing options based exclusively on interest rates, disregarding critical factors like loan flexibility, potential tax implications, and overall financial sustainability.

Successful real estate investors approach financing as a strategic decision that requires thorough research, professional consultation, and a holistic understanding of their investment objectives.

Pro tip: Create a detailed financial spreadsheet comparing all loan options, including total costs over the entire loan term, not just initial interest rates.

Unlock Smarter Financing for Your Real Estate Investment Journey

Navigating the complex world of investor financing, including loan types like conventional, private, and creative loans, can feel overwhelming. Many investors struggle with understanding loan terms, managing risk, or finding trustworthy lenders who fit their unique financial profiles. Whether you are exploring how to calculate your debt service coverage ratio or seeking expert guidance on securing the best loan-to-value ratios for your investment properties, the right support can transform your approach.

Discover how Bold Street AI simplifies this process by connecting you with investor-friendly lenders, agents, and property managers all in one place. Access curated financing options tailored to your needs and leverage educational tools that demystify complex real estate financing concepts. Start building your wealth confidently with expert mentorship and a vibrant community ready to share strategies. Take the first step to make your financing work for you right now by visiting Bold Street AI and exploring tailored real estate investment solutions.

Frequently Asked Questions

What are the main types of financing options available for real estate investors?

Investor financing options include conventional loans, private money loans, hard money loans, and creative financing strategies like seller financing and lease options. Each has its own advantages and drawbacks depending on the investor’s financial profile and investment goals.

How can I determine my eligibility for real estate investment loans?

Eligibility typically hinges on factors like credit score, income stability, debt-to-income ratio, and previous investment performance. Most lenders look for a credit score of 680 or higher, with documentation of steady income for the past two years.

What is the importance of understanding loan terms in real estate financing?

Understanding loan terms is crucial to avoid pitfalls such as hidden fees, prepayment penalties, and interest rate adjustments. Misunderstanding these details can lead to unexpected costs and impact your overall investment profitability.

How can I manage risks and costs associated with real estate investments?

To manage risks and costs, investors should develop a comprehensive financial plan that includes maintaining an emergency fund, anticipating maintenance and vacancy expenses, and consulting with financial professionals to navigate tax implications.

Recommended

- 2024 is the Perfect Time to Become a Real Estate Investor – Bold Street AI

- Navigating the Terrain: Common Challenges for Real Estate Agents Working with Residential Real Estate Investors – Bold Street AI

- Discover The Secret Investment Playbook of Residential Real Estate – Bold Street AI

- Blog – Bold Street AI

- Financing | R & R Swimming Pools