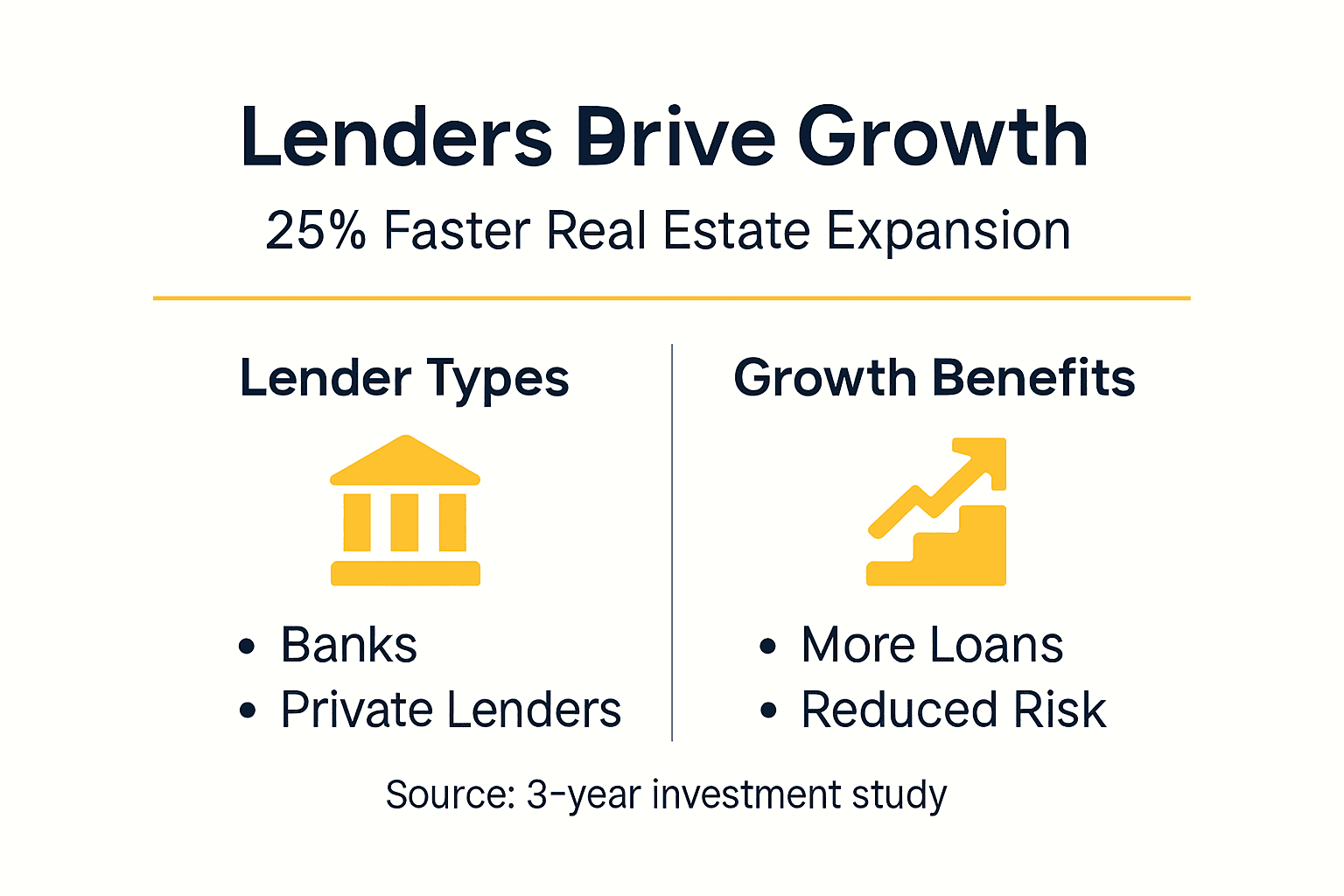

Investors who mix traditional and private lender financing grow their portfolios 25% faster over three years compared to those sticking to one source. Yet many new investors struggle to understand which lenders suit their goals or how to navigate qualification criteria. This guide reveals how lenders influence your success, what loan products exist, and how to leverage financing diversity to accelerate your real estate portfolio confidently.

Table of Contents

- Introduction To Lenders In Real Estate Investing

- Types Of Lenders And Loan Products For Real Estate Investors

- Lender Qualification Criteria And Impact On Investment Feasibility

- Common Misconceptions About Lenders In Real Estate Investing

- Building Strong Lender Relationships To Enhance Financing Success

- Leveraging Lender Options To Maximize Real Estate Portfolio Growth

- Conclusion: Applying Lender Knowledge For Confident Real Estate Investing

- Boost Your Real Estate Investing Success With Bold Street AI

- Frequently Asked Questions About Lenders In Real Estate Investing

Key Takeaways

| Point | Details |

|---|---|

| Lenders shape investment success | Different lender types offer varied loan products and criteria that directly impact your ability to acquire properties and grow your portfolio. |

| Creditworthiness matters significantly | Credit scores, debt-to-income ratios, and reserve funds are key factors lenders evaluate when approving loans and setting terms. |

| Common myths mislead investors | Misconceptions about down payments, FHA loans, and hard money lenders often prevent new investors from exploring viable financing options. |

| Relationships improve loan outcomes | Building trust with lenders leads to better terms, faster approvals, and stronger negotiation power for future deals. |

| Diversification accelerates growth | Using multiple financing sources reduces risk and can increase portfolio expansion speed by 25% over three years. |

Introduction to Lenders in Real Estate Investing

Financing is the backbone of real estate investing. Most investors cannot purchase properties outright with cash. They rely on lenders to provide necessary capital that enables property acquisition and determines investment feasibility through loan structures.

Three main lender categories dominate the landscape. Traditional banks offer conventional mortgages with strict qualification requirements. Private lenders provide flexible terms tailored to individual deals. Credit unions deliver personalized service with competitive rates for members.

Each lender type has unique characteristics affecting how easily you access funds and what they cost. Banks typically offer lower interest rates but demand excellent credit and extensive documentation. Private lenders focus more on property value than borrower credentials, making them ideal for quick transactions or unconventional deals.

Understanding these distinctions helps you match financing sources to your investment strategy. A fix-and-flip investor might prioritize speed and choose hard money loans despite higher costs. A buy-and-hold investor might prefer conventional loans for their lower long-term expenses.

“The right lender relationship can mean the difference between closing a profitable deal and watching it slip away to competitors.”

Exploring real estate financing options early in your investing journey positions you to act decisively when opportunities arise. The foundation you build now determines how quickly you can scale your portfolio later.

Types of Lenders and Loan Products for Real Estate Investors

Conventional loans from traditional banks remain the most common financing vehicle. These mortgages require credit scores typically above 620 and debt-to-income ratios below 43%. Borrowers must demonstrate stable income and employment history. Interest rates are competitive, often ranging from 6% to 8% in 2026, making them cost-effective for long-term holds.

Hard money loans operate differently. These asset-based products focus on property value rather than borrower creditworthiness. Approval happens quickly, sometimes within days, because lenders primarily evaluate the collateral. Expect higher interest rates of 10% to 15% and shorter terms of 6 to 24 months. Real estate flippers favor hard money for speed despite the premium cost.

Private lenders and credit unions offer middle-ground solutions. Private lenders are individuals or small groups who fund deals directly, often with flexible qualification standards and negotiable terms. Credit unions provide conventional-style loans but with more personalized service and potentially lower rates for members. Both options suit investors who need customized financing structures.

FHA loans deserve special attention for new investors. These government-backed mortgages allow down payments as low as 3.5% and finance multi-family properties up to four units if you occupy one as your primary residence. This creates an accessible entry point for house hacking strategies that generate rental income while building equity.

| Loan Type | Typical Rate | Down Payment | Best For |

|---|---|---|---|

| Conventional | 6-8% | 15-25% | Long-term rentals with strong credit |

| Hard Money | 10-15% | 10-20% | Quick flips and time-sensitive deals |

| FHA | 6-7% | 3.5% | Owner-occupied multi-family starters |

| Private Lender | 8-12% | Varies | Flexible terms and unique properties |

Matching loan products to your investment goals requires understanding these trade-offs. Explore financing options for real estate investors to identify which products align with your strategy and financial position. Consider consulting resources on financing options for investors to build a diversified approach.

Lender Qualification Criteria and Impact on Investment Feasibility

Credit scores and debt-to-income ratios form the foundation of lender evaluations. Most conventional lenders require scores above 620, though better rates await those above 740. Your debt-to-income ratio measures monthly debt payments against gross income. Lenders prefer ratios below 43%, though some accept up to 50% with compensating factors like substantial reserves.

Proof of reserves matters significantly. Lenders want evidence you can cover several months of mortgage payments, property expenses, and personal obligations even if rental income disappears. Expect to show bank statements demonstrating liquid assets equal to six months of combined expenses for investment properties.

Property characteristics influence risk assessments too. Single-family homes in stable markets receive favorable treatment. Multi-family properties, commercial spaces, or homes in declining areas may face stricter scrutiny or higher rates. Location impacts everything. Properties in economically vibrant regions with low vacancy rates get approved more easily than those in struggling markets.

These qualification standards directly affect your investment capacity. Strong credit and low debt ratios unlock better terms, lower rates, and higher loan amounts. Weak financials limit options to expensive hard money or force you to find creative partnerships.

Pro Tip: Maintain reserves equal to at least six months of expenses and keep your debt-to-income ratio below 40% to maximize lender confidence and secure optimal terms.

Understanding how lenders assess investment viability empowers you to prepare financially before applying. Review lender qualification criteria to identify areas needing improvement and develop a timeline for meeting standards that unlock growth opportunities.

Common Misconceptions About Lenders in Real Estate Investing

The 20% down payment myth persists despite abundant evidence otherwise. Many conventional loans accept 15% down for investment properties. Some portfolio lenders go as low as 10%. FHA loans for owner-occupied multi-family properties require just 3.5%. This misconception prevents new investors from exploring accessible entry strategies.

Another widespread belief claims FHA loans cannot finance investment properties. Wrong. FHA loans can finance multi-family properties up to four units if the borrower occupies one unit as a primary residence. This house hacking approach generates rental income while qualifying for favorable FHA terms. It represents one of the most powerful strategies for beginners.

Hard money loans carry a reputation as desperate options for poor credit borrowers. Reality differs. Real estate professionals use hard money strategically for speed and convenience, not credit deficiencies. When a profitable flip opportunity requires closing in days, hard money provides the necessary velocity despite higher costs. The premium often pays for itself through faster returns.

Many assume credit scores alone determine approval. Lenders actually evaluate comprehensive financial pictures including property specifics, borrower reserves, and investment experience. A lower credit score paired with substantial cash reserves and profitable property analysis might outperform a higher score with thin margins.

Understanding true FHA loans for investment properties capabilities opens doors many investors overlook. Challenge these misconceptions by researching actual lender requirements and speaking directly with multiple financing sources about realistic qualification paths.

Building Strong Lender Relationships to Enhance Financing Success

Building trust and rapport with lenders creates tangible advantages. Established relationships lead to faster approvals, better terms, and increased flexibility when unusual situations arise. Lenders prefer working with borrowers they know and trust, especially for investment properties where risk assessment involves more variables.

Consistent communication forms the foundation. Update lenders on your investment activities even when not actively seeking loans. Share successes, property performance data, and portfolio growth. This ongoing dialogue keeps you top of mind when new loan products or favorable terms become available.

Timely documentation delivery demonstrates professionalism. When lenders request tax returns, bank statements, or property analyses, respond within 24 hours. Organized, complete submissions signal competence and reduce processing delays. Create a digital folder system with all standard documents ready for instant sharing.

Honesty about financials builds credibility. Disclose challenges transparently rather than hiding problems that underwriting will uncover anyway. Lenders appreciate straightforward communication and often help problem-solve when they understand situations fully. Attempting to obscure difficulties destroys trust permanently.

Repeat business strengthens negotiation power. After successfully completing one loan and demonstrating reliable performance, approach the same lender for subsequent deals. Proven track records justify requests for reduced rates, lower down payments, or expedited processing. Each successful transaction compounds your credibility.

Pro Tip: Keep organized financial records updated quarterly including profit and loss statements, rent rolls, and property valuations to impress lenders and streamline future loan applications.

Learn to build lender relationships systematically by treating financing partners as long-term collaborators rather than transactional service providers. These strategic alliances become force multipliers for portfolio expansion.

Leveraging Lender Options to Maximize Real Estate Portfolio Growth

Diversifying financing sources accelerates portfolio expansion while reducing risk. Banks offer stability and low rates for long-term holds. Private lenders provide flexibility for unique properties or creative deal structures. Hard money lenders enable quick acquisitions when timing matters more than cost. Combining these sources strategically positions you to capitalize on varied opportunities.

Research demonstrates investors mixing traditional and alternative financing grow portfolios 25% faster over three years compared to single-source strategies. This advantage stems from matching optimal financing to each deal’s characteristics rather than forcing every property into identical loan products.

Practical steps begin with honest self-assessment. Calculate your current credit score, debt-to-income ratio, and available reserves. These metrics determine which lenders will approve you and what terms to expect. Next, research multiple lenders across all categories. Interview at least three banks, two private lenders, and one hard money source to understand options comprehensively.

Mix traditional and alternative loans intentionally. Use conventional mortgages for stable, cash-flowing rentals where low rates maximize long-term returns. Deploy hard money for fix-and-flip projects where speed creates profit. Explore private lenders for properties that don’t fit traditional molds but offer solid returns.

Mitigating risk through diversification prevents single points of failure. Relying exclusively on one bank means their policy changes or portfolio constraints could halt your growth. Maintaining relationships with multiple financing sources ensures alternatives exist when primary options become unavailable.

| Lender Type | Advantage | Best Use Case | Growth Impact |

|---|---|---|---|

| Traditional Banks | Lowest rates, stable terms | Long-term rentals | Foundation for steady cash flow |

| Private Lenders | Flexible qualification | Unique properties | Access to deals others miss |

| Hard Money | Speed, asset-based | Time-sensitive flips | Rapid capital recycling |

Explore financing source diversification to develop a balanced approach that supports multiple investment strategies simultaneously. This comprehensive financing foundation positions you to act decisively across market conditions.

Conclusion: Applying Lender Knowledge for Confident Real Estate Investing

Lenders play pivotal roles in real estate investing success. Understanding the different types, from traditional banks to private lenders and hard money sources, empowers you to match financing with investment strategies. Qualification criteria like credit scores, debt-to-income ratios, and reserves directly impact your access to capital and the terms you receive.

Common misconceptions about down payments, FHA loans, and hard money products often prevent new investors from exploring viable paths. Challenging these myths opens opportunities many overlook. Building strong lender relationships through consistent communication, organized documentation, and transparent dealings creates advantages that compound over time.

Diversifying financing sources can accelerate portfolio growth by 25% while reducing risk. Apply this knowledge by assessing your current financial position, researching multiple lender types, and strategically matching loan products to specific deals. Prepare financially by improving credit, reducing debt, and building reserves that position you as a preferred borrower.

Your next step is taking action. Connect with lenders, explore financing options actively, and start building relationships that will support your investing journey. The knowledge you’ve gained here transforms from information into results only through application. Begin today.

Boost Your Real Estate Investing Success with Bold Street AI

Navigating lender relationships and financing options becomes simpler with the right support system. Bold Street AI connects residential real estate investing beginners with investor-friendly lenders who understand your goals and offer tailored solutions.

Our platform helps you explore comprehensive financing options for investors while providing educational resources through Bold Academy. Access tools that streamline property analysis, connect with experienced mentors, and join a community of investors sharing insights and strategies. Whether you’re securing your first loan or diversifying financing for portfolio expansion, Bold Street AI offers the guidance and connections you need. Follow our investing workflow guide to build confidence and accelerate your path from beginner to successful investor.

Frequently Asked Questions About Lenders in Real Estate Investing

What credit score do I need to get a real estate investment loan?

Most conventional lenders require credit scores above 620 for investment property loans, though scores above 740 unlock the best rates and terms. Hard money lenders focus primarily on property value rather than credit scores, making them accessible even with lower scores. Building your score above 700 before applying improves approval odds and reduces costs significantly.

Can I use FHA loans for investment properties?

Yes, FHA loans can finance multi-family properties up to four units if you occupy one unit as your primary residence. This house hacking strategy allows new investors to start with just 3.5% down while generating rental income from the other units. It represents one of the most accessible entry points for beginners with limited capital.

How can I improve my chances of loan approval?

Focus on three key areas: boost your credit score above 700, reduce your debt-to-income ratio below 40%, and build cash reserves covering at least six months of expenses. Additionally, prepare organized financial documentation and develop relationships with multiple lenders before you need loans. Demonstrating investment knowledge through education and clear property analysis also strengthens applications.

What benefits do private lenders offer to new investors?

Private lenders provide more flexible qualification standards than traditional banks, focusing on deal quality rather than rigid credit requirements. They offer faster approval processes, often within days, and create customized loan structures matching your specific investment needs. Many private lenders also mentor new investors, sharing market insights and property evaluation guidance that accelerates learning.

Is it necessary to have a 20% down payment for investment loans?

No, 20% down payments are not universally required. Many conventional loans accept 15% down for investment properties, some portfolio lenders go as low as 10%, and FHA loans for owner-occupied multi-family properties require just 3.5%. Hard money lenders typically require 10% to 20% but focus more on property value than borrower down payment capacity.

Recommended

- Financing Options for Investors: Building Wealth in Real Estate | Bold Street AI

- Best Financing Solutions for Real Estate Investors 2026 | Bold Street AI

- 6 Examples of Financing Options for Real Estate Investors | Bold Street AI

- Predicted Fed Rate Cuts in 2024: Implications for the Real Estate Market and Investor Strategies | Bold Street AI

- Own CE Content: 100% IDCEC Approval & 10x ROI Boost